A strong bounce back by automotive manufacturers

In this section, Grant Thornton provides an overview of the current manufacturer landscape including the latest profit reports and factors affecting new car production.

Continue reading

Owen Edwards, Associate Director

at Grant Thornton UK LLP

Over the last 24 months, the automotive industry has undergone several extreme changes. In the upstream (manufacturing), the supply chain and production processes have been reviewed in a bid to cope with the closure of factories and reduce costs in order to enhance earnings. Downstream (dealers and customer facing companies), have also experienced rapid change, forcing the industry to retail online; this is a process that had threatened the industry for some years but did not appear until the Covid-19 pandemic. In this article, we are examining the impact of the pandemic on the upstream automotive industry.

The automotive upstream industry is a global system, using just-in-time supply chain processes to source components for vehicles across a broad number of continents in order to

maintain working capital/inventory to a minimum, normalise trapped cash in the business, and maintain lower costs in the production process. The effects of the global pandemic are far from over as we can see with the spread of new Covid-19 variant to the shortage in semiconductors and other vehicle components such as raw materials. However, we have looked back over the period from the start of 2020 to the most recently reported quarter (calendar Q1 2021) to see how OEMs have adapted to the impact of the pandemic.

The early part of the first quarter of 2020 saw limited impact on the profits of most major OEMs. There was also limited impact to the supply chain, with small amounts of disruption, especially in China where the pandemic first took hold. However, by mid Q1, this was to change, and factories closed as lockdowns were imposed around the world. By the end of the Q1 2020, most of Europe was in lockdown or was considering lockdown. By Q2 2020, profits were falling dramatically and, in some cases, tipping into significant losses (we have used normalised earnings as this does not account for any exceptional items that may have affected profits). General Motors, Toyota, Kia, Tesla and Hyundai remained in profit in Q2 2020; however, Hyundai went on to make a loss in Q3 2020, slightly later than some of its competitors.

OEM profitability profile - Q1 2019 to Q1 2021

Source: Thompson Reuter

"OEMs have bounced back strongly, underpinned by a mix of improving volumes, better market conditions, increased plant utilisation, and cost reductions. The strength of the rebound has been unexpected, exceeding that of Q1 2019."

Owen Edwards, Associate Director at Grant Thornton UK LLP

OEM Q2 2020 normalised EBIT

Source: Thompsons Reuters

With factories closed and the retailing of vehicles also on hold, there was little OEMs could do to stop their profits from being impacted. Cost reductions were quickly put into place and staff put on furlough where possible. Tesla continued to make a profit, delaying the closure of production in its Fremont plant in the US for as long as possible and reopening production as quickly as possible when it could. The business also quickly diverted production to its plant in China. However, caution is needed when using normalised numbers as the business continued to benefit from other OEMs purchasing Regulatory Credits (also known as environmental credits). Therefore, removing the income from Regulatory Credits to leave only income generated from the production of vehicles, the business was in loss over the period of Q1 and Q2 2020. Vehicles produced nevertheless continued to increase and it was not until Q3 that Tesla’s normalised EBIT ex Regulatory Credits started to make profits. Even excluding regulatory credits, this was a strong rebound for a such a young OEM.

Tesla normalised EBIT including and excluded Regularity Credits Q1 2020 to Q1 2021

Source: Tesla Inc

OEMs responded quickly to the change in the market by making cost reductions. Despite having made losses in Q2 2020 of US$6.1bn, Ford’s performance improved in Q3 with a strong rebound to US$2.8bn profit caused by its focus on high-value vehicles such as SUVs and pickup trucks, which enjoyed a strong increase in demand after the pandemic’s initial impact. Furthermore, Ford’s cost reduction plan, which started in 2017/18, started to realise value.

Stellantis also experienced a strong rebound from a US$0.96bn loss to US$2.2bn profits in Q3 2020. Stellantis benefited from continued cost reductions from its recent acquisitions of Opel/Vauxhall and FCA.

However, Nissan Motor Company was heavily affected by the lack of production in calendar Q1 and Q2 2020, making large losses of US$94bn and US$153bn respectively. Nissan was already struggling in the US market before the pandemic and this was compounded by the drop in production over Q1 and Q2 2020. Nevertheless, the cost reductions meant that the business generated less severe losses than investors had expected. Further cost cutting took place over the period and vehicle volumes returned; by Q3 2020 Nissan was making a profit.

Honda and Mazda both followed a similar trend, with Honda becoming profitable in Q3 2020 and Mazda following in Q4 2020.

As 2020 ended and Q1 2021 began, most of the OEMs were generating profits, with the exception of Nissan.

The following chart provides an indication of the trend of the combined OEMs’ profits and losses over the period Q1 2019 to Q1 2021 (includes the following companies: Hyundai, KIA, Toyota, Tesla, General Motors, BMW, VW, Stellantis, Ford, Mazda, Honda and Nissan. Renault is not included as they do not provide quarterly results. Furthemore for clarity, Stellantis has not provided normalised EBIT for Q1 2021 and this should be considered when comparing the Q1 2021 figures to Q4 2020 and Q1 2019).

Combined OEM normalised EBIT from Q1 2019 to Q1 2021

Source: Thompson Reuter and company websites

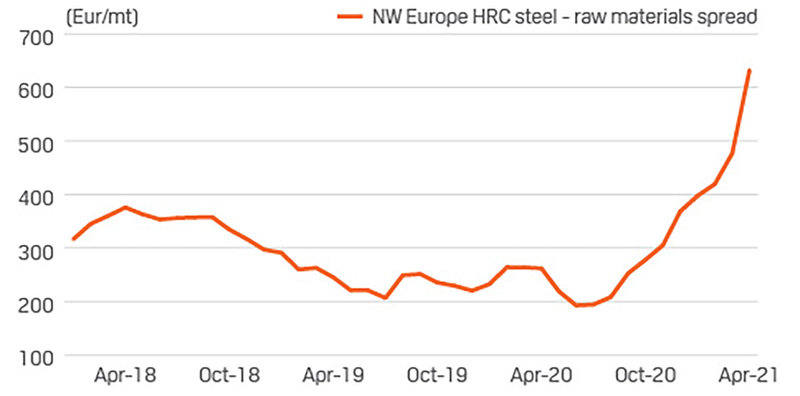

As can be seen from the chart, OEMs have bounced back strongly, underpinned by a mix of improving volumes, better market conditions, increased plant utilisation, and cost reductions. The strength of the rebound has been unexpected, exceeding that of Q1 2019 (Q1 2021 does not include a EBIT figure for Stellantis). How will 2021 end? It is difficult to say; after a strong performance in Q1 2021, there is increasing evidence of supply chain issues, shortages of raw materials and high raw material prices, which could affect the price and supply of new vehicles. The demand for hot rolled coil steel used in the automotive industry for chassis has increased significantly in 2021. The following S&P chart shows signficant growth in the price in steel.

Semiconductor shortages have also created supply issues that could lead to further plant closures, such as BMW Mini in Oxford. Alix Partners has suggested that the shortage in semiconductors could reduce OEMs’ revenue by US$110bn in 2021. The automotive OEMs are resistant to disruption and adversity; demand for vehicles is holding up well and this can be attributed to the way vehicles are sold. Vehicle financing is key to the current market demand. In the UK over 80% of all cars are financed through Personal Contract Purchase (PCP) and this has enabled potential buyers of vehicles to make manageable monthly payments on vehicles. Furthermore, a prolonged period of low interest rates has made borrowing affordable, and demand is expected to continue in 2021, with vehicle shortages also helping to maintain high prices for both the new and used car market which in turn generates strong margins for the OEMs and their importation and distribution businesses.

A number of the OEMs are working through their cost-cutting strategies to generate efficiency gains and this is likely to support profitability towards the end of 2021. Therefore, the next six months is expected to prove buoyant for some OEMs, and although supply chain issues may cause problems, profits are expected to hold up well. There is a clear indication in both the supply chain and distribution of vehicles that the automotive industry can react quickly and adapt to change, however as highlighted by the semicondutor shortage, the just-in-time supply chain approach which has worked for many years has struggled in the current unknown environment.

Share

Fuel/insight